The 2024 Australian vintage was most distinctive for the increase in tonnage and share of white varieties, while reds – and Shiraz in particular – were well down on their long-term average crush.

This market bulletin by Wine Australia looks at whether the latest retail sales figures for the Australian domestic market reflect these same trends, and identifies which varieties are most in demand.

This comparison of trends in the crush and retail sales indicates that the Australian wine sector is responding to market trends and taking advantage of growth opportunities.

Despite a 20-year low crush in 2023, the crush of red grapes declined by a further one percent in 2024, taking it to its lowest level since 2007.

Shiraz drove the decline – down by nearly 48,000 tonnes nationally (the equivalent of around four million nine-litres cases) compared with the previous year.

However, given that 2023 was such a low vintage, a better indicator of demand-driven growth as opposed to seasonal variation is to compare the 2024 crush with 2022, which was an average-sized vintage.

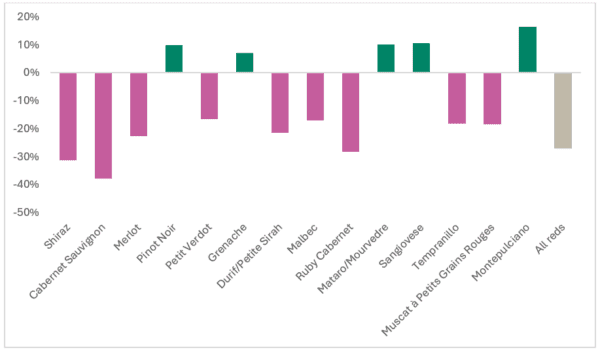

Looking at the major red varieties, the ones in growth over the two years were Pinot Noir, Grenache, Mataro (Mourvèdre), Sangiovese and Montepulciano, all of which showed positive growth despite the overall red crush declining by 27 percent and both Shiraz and Cabernet Sauvignon declining by over 30 percent each (see Figure 1).

Figure 1. Percentage change in crush for major red varieties from 2022 to 2024. Source: Wine Australia National Vintage Survey (varieties sorted by crush size in 2024).

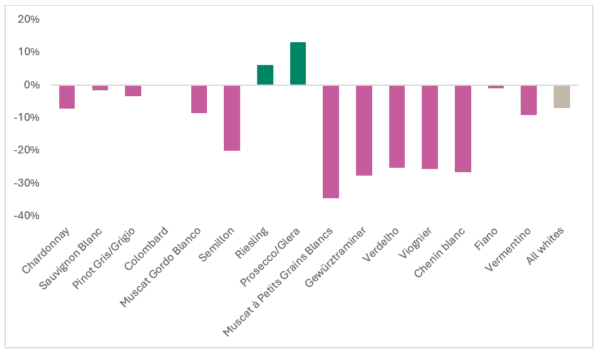

Looking at white varieties, there was an overall decline of seven percent in 2024 compared with 2022, and almost every variety decreased.

Only Riesling (up six percent) and Prosecco (up 13 percent) have shown growth over the two years; however, the declines for Sauvignon Blanc (down two percent), Pinot Gris/Grigio (down three percent) and Fiano (down one percent) were all smaller than the overall figure, indicating a counteracting trend (Figure 2).

Figure 2. Percentage change in crush for major white varieties from 2022 to 2024. Source: Wine Australia National Vintage Survey) varieties sorted by crush size in 2024).

On the domestic market, retail sales data from Circana for the year ended 30 June 2024 is broadly consistent with the crush data in terms of the best-performing varieties.

Overall, wine sales declined by two percent, driven by still red varieties, which were down three percent year-on-year in volume, while whites were flat.

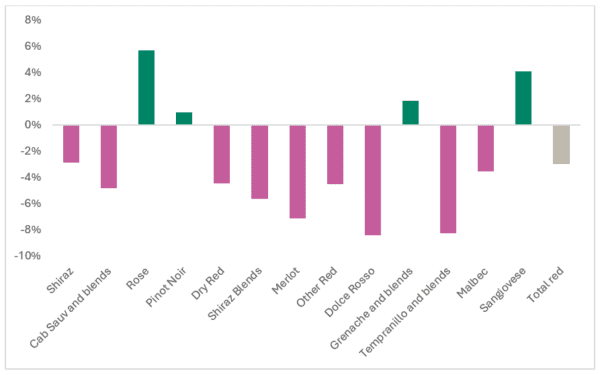

The only red varieties showing volume growth over the 12-month period were Grenache (up three percent), Pinot Noir (up one percent) and Sangiovese (up four percent) – mirroring the growth in varieties crushed shown in Figure 1.

The exception was Mataro/Mourvèdre (down 46 percent in the retail figures) while Montepulciano is not separately identified in the Circana data. Shiraz was down three percent, Cabernet Sauvignon (including blends) down five percent and Merlot down seven percent (Figure 3).

Figure 3. Percentage change in off-trade retail sales for major red varieties (YE June 2024). Source: Circana (varieties sorted by sales volume).

Rosé has been classified as a red variety in the sales figures, but can’t be directly related to a particular variety in the crush data. This category grew by six percent, consistent with a growing demand for lighter styles of wine.

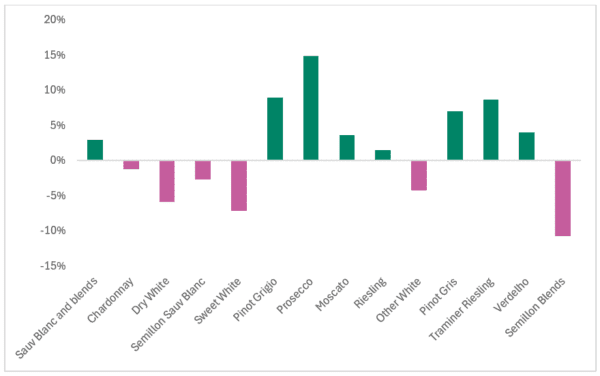

The performance of the white varieties in the retail data was better overall than in the crush data, with more than half of the major still white varieties in growth (Figure 4).

As in the case of the crush, Prosecco (up 15 percent), Pinot Gris and Pinot Grigio (up nine percent as a combined category), Sauvignon Blanc (up three percent) and Riesling (up one percent) were among the best performers.

An exception was Moscato, which grew by four percent whereas the crush of the main Muscat varieties (Muscat a Petits Grains Blanc and Muscat Gordo Blanco) was down by 16 percent overall in 2024 compared with 2022.

Traminer Riesling (Gewürztraminer) and Verdelho were other strong performers in the retail figures (up nine percent and four percent respectively) where the crush figures did not reflect this growth.

Figure 4. Percentage change in off-trade retail sales for major white varieties (YE June 2024). Source: Circana (varieties sorted by sales volume).

It should be noted that these percentage growth figures are often from a small base.

Absolute declines in larger categories (e.g. dry white and Chardonnay) have offset the increases in these other varieties, giving an overall flat result and showing that there is not a strong underlying demand for more white wine that would drive demand for any further increase in the grape crush.

This finding is also consistent with the fact that the crush in 2024 was nearly 20 percent below its 10-year average, and the third time in five years that it has been below average.

Overall, this comparison of trends in the crush and retail sales indicates that the Australian wine sector is responding to market trends and taking advantage of growth opportunities.

Related content

Recent Comments